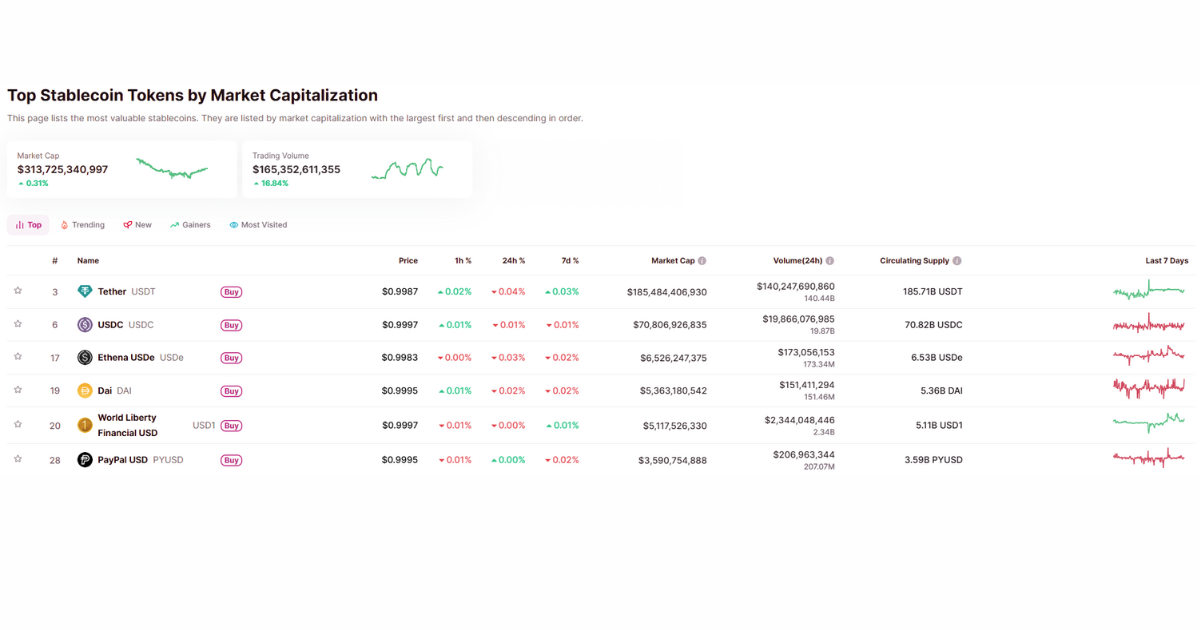

Bitcoin dropped 33% in three weeks. Ethereum followed. But one cryptocurrency barely budged, and it’s now bigger than many regional banks. Stablecoins have quietly surged past $255 billion, becoming one of the largest holders of U.S. Treasury bills. They promise the speed of crypto without the wild price swings. Compare stats at CoinGecko Stablecoin Data.

But here’s the catch: “stable” isn’t the same as “safe.” And recent collapses prove why American investors need to understand what they’re actually buying.

What Stablecoins Actually Are

A stablecoin is a cryptocurrency designed to keep a fixed $1 value. Think of it as crypto’s attempt at creating a digital dollar. Learn more at Investopedia: Stablecoin.

The mechanism is straightforward: companies issue digital coins and hold real dollars or Treasury bills in reserve. When you want to cash out, they redeem your coin for $1 from these reserves. If you’re new to how blockchains work, check out our Beginner’s Guide to Blockchain Technology in 2026.

The Three Types That Matter

Fiat-backed stablecoins like Tether (USDT) and USD Coin (USDC) are backed by actual dollars in bank accounts. These control 90% of the market. Tether alone has $155 billion in circulation. Official issuers: Tether (USDT) | USD Coin (USDC).

The problem? Transparency varies wildly. USDC publishes monthly audits from Grant Thornton. Tether has been far less transparent about its reserves.

Crypto-backed stablecoins like DAI use other cryptocurrencies as collateral. More decentralized but technically riskier; if the backing crypto crashes fast enough, the system can fail. Learn about DAI at MakerDAO.

Algorithmic stablecoins use code instead of reserves. These have the worst track record. TerraUSD collapsed in May 2022, wiping out $40 billion. USDe dropped to 65 cents in October 2025, a 35% instant loss. News coverage: USDT stablecoin as governments wobble

Bottom line: Stick with fiat-backed options from established issuers. Avoid algorithmic stablecoins entirely.

When Stablecoins Have Failed Americans

March 2023: USDC plunged to 87 cents after $3.3 billion got trapped in Silicon Valley Bank’s collapse. If you were using USDC for a payment that day, you instantly lost 13% of your purchasing power.

May 2022: TerraUSD collapsed completely, dropping from $1 to near-zero. American investors lost billions.

October 2025: USDe crashed to 65 cents during market stress, triggering $20 billion in crypto liquidations.

The pattern is clear: even major stablecoins can lose their peg when markets panic. More than one-third of all stablecoins ever launched have failed completely . Check CoinMarketCap Stablecoins for up-to-date market caps.

Source Image: CoinMarketCap

New U.S. Regulation: Better, But Not Perfect

In July 2025, President Trump signed the GENIUS Act, America’s first comprehensive stablecoin law. It requires issuers to maintain full reserves in cash and Treasury bills, allow on-demand redemption at $1, publish regular audits, and register with federal regulators. Read more: GENIUS Act Summary

But experts have identified critical loopholes.

The law prohibits stablecoin companies from paying interest directly. But third parties still can create bank-run risk, which the law was supposed to prevent. During market stress, DeFi lending platforms can freeze withdrawals indefinitely.

Former SEC cryptocurrency policy expert Corey Frayer warned, “We now have private companies issuing what essentially are private dollars,” a system America abandoned after the Civil War because of repeated financial panics. Investigate whether the stablecoin law allows crypto firms.

The Systemic Risk to U.S. Markets

Tether and Circle (USDC’s issuer) now rank among the top 20 holders of U.S. Treasury bills.

If these stablecoins experienced a run of millions trying to cash out simultaneously, issuers would need to dump massive amounts of Treasuries quickly. A fire sale could disrupt Treasury markets and affect interest rates across the American economy.

For deeper context on how digital finance trends interact with traditional systems like tax rules and government payments, see our article on Economic Impact Payments vs. IRS Tax Refunds.

The European Central Bank warned in November 2025 that this systemic risk grows as the stablecoin market cap heads toward $2 trillion by 2028.

Where Stablecoins Actually Make Sense

Even with some risks, stablecoins can be very useful:

Cheaper international transfers: Sending $200 to Mexico via Western Union costs about $9.60. Using a stablecoin, the same transfer costs around $1–2, saving 80–90%.

Faster business payments: Some U.S. companies use stablecoins for quicker international settlements at lower costs than traditional SWIFT transfers.

Crypto trading: The primary use case, letting traders exit volatile positions without converting back to dollars through traditional banking.

These benefits explain why stablecoins aren’t disappearing. The question is making them actually safe.

How to Protect Yourself: Investor Checklist

Use this checklist to easily identify safe stablecoins and avoid risky ones.

Reserve Transparency: Look for monthly reports from top accounting firms showing exactly what backs the coin.

Red flag: Vague statements or “trust us” marketing.

U.S. Regulatory Status: Check for registration with FinCEN or approval from the New York Department of Financial Services.

Red flag: Companies based offshore with little or no oversight.

Reserve Quality: Make sure reserves are in cash or U.S. Treasury bills.

Red flag: Reserves in commercial paper or corporate bonds that could lose value.

Track Record: Choose stablecoins with a multi-year history of protecting investors during market stress.

Red flag: Delayed or suspended withdrawals.

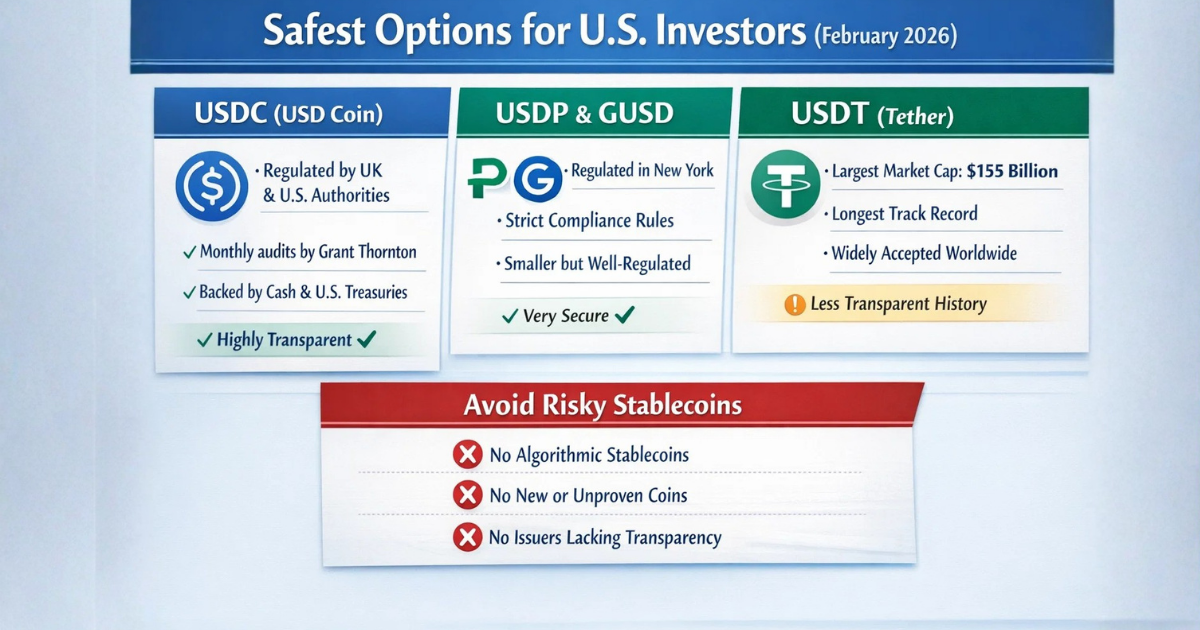

Safest Options for U.S. Investors (February 2026)

For U.S. investors, safety matters most when choosing a stablecoin. In February 2026, these stablecoins are known for strict rules, clear reserve reports, and a reliable track record.

USDC (USD Coin): Regulated by UK and U.S. authorities. It releases monthly reports from Grant Thornton and is backed mainly by cash and U.S. Treasury assets. It is one of the most transparent stablecoins.

USDP and GUSD: Regulated in New York with strict rules. Smaller but very well-regulated.

USDT (Tether): Largest market cap ($155 billion), longest track record, most widely accepted. But historically, it has been less transparent about reserves.

Avoid algorithmic stablecoins, new coins without track records, and any issuer that refuses to be transparent.

Don’t Say We Didn’t Warn You

Stablecoins aren’t going to revolutionize finance tomorrow. They’re not going to replace the dollar. And they’re definitely not “risk-free” just because the price is supposed to stay at $1.

They’re a useful tool for specific situations. Nothing more, nothing less.

If you’re using stablecoins to send cheaper remittances abroad or you’re a trader moving in and out of positions, fine. But if you’re treating them like a savings account because someone promised 8% risk-free yield? You’re the exit liquidity everyone else is looking for.

The Fed, Treasury, and banking regulators are watching carefully. They’re not panicking, but they’re not thrilled either. The new regulations are a start; they’re not enough. More will come, probably after the next crisis makes headlines.

Use stablecoins if they solve a specific problem for you. But keep your serious money where it’s actually protected in boring, FDIC-insured accounts that don’t crash to 87 cents on random weekends.

Remember: “Stable” describes what it’s supposed to do. “Risky” describes what it actually is.

Invest accordingly.

For more practical tips and guides on managing your money safely in 2026, visit Financecurves and stay ahead of the curve.

FAQs

What are stablecoins?

Stablecoins are a type of cryptocurrency designed to maintain a stable value by being pegged to assets like the U.S. dollar, other fiat currencies, or commodities — offering a less volatile alternative to typical crypto tokens.

Do stablecoins guarantee safety for investors?

No, while stablecoins aim to reduce price volatility, they aren’t completely risk-free. Their safety depends on reserve backing, issuer transparency, and market conditions. ◆

What risks do stablecoins face?

Stablecoins can face reserve transparency issues, depeg events if backing assets lose value, regulatory uncertainty, and technical vulnerabilities (especially in algorithmic models).

Are all stablecoins backed by real dollars?

Not always. Some stablecoins are fiat-backed, with reserves held in bank accounts, while others are backed by crypto assets or use algorithms to maintain their peg — and each backing method carries different levels of risk.

Can stablecoins be used safely for payments and transfers?

Stablecoins can offer fast, lower-fee transfers compared with traditional finance and are widely used in DeFi and cross-border payments, but users should assess issuer reliability, legal compliance, and the platform where they hold the stablecoin.

Disclaimer

The information provided on this website is for informational and educational purposes only. While we strive to ensure accuracy and keep our content up to date, FinanceCurves makes no guarantees regarding the completeness, reliability, or accuracy of any information published.

Nothing on this site constitutes financial, tax, legal, or investment advice. Readers should consult a qualified financial advisor, certified tax professional, or licensed attorney before making any financial decisions. Your individual situation may vary, and decisions based on information from this website are made at your own risk.

FinanceCurves may reference government agencies, financial institutions, or official programs for informational purposes only. We are not affiliated with, endorsed by, or connected to any government entity, including the IRS or any federal or state agency. Some content may contain links to third-party websites for additional context or resources. We are not responsible for the content, accuracy, or practices of any external sites.

By using this website, you agree to this disclaimer and our terms of use.

Marshall Mason, Senior Market Analyst at FinanceCurves.com, has over 9 years of experience covering financial markets, cryptocurrencies, and macroeconomic trends. He delivers data-driven insights, independent analysis, and actionable guidance for investors and traders. Marshall leverages authoritative sources, market data, and regulatory updates to help readers navigate volatility, adoption trends, and the evolving landscape of global finance and digital assets.