Big Beat, Bigger Questions

Microsoft’s Q2 earnings 2026 report delivered exactly what Wall Street usually loves—strong revenue growth, rising profits, and booming cloud sales. Yet, instead of rallying, Microsoft shares fell sharply in after-hours trading, raising a key question for investors: Why did the market punish such strong results?

The answer lies in aggressive AI investment, rising capital expenditures, and expectations around future margins. While Microsoft’s fundamentals remain strong, investors are clearly recalibrating how much they are willing to pay for AI-driven growth.

Here’s a clear, data-backed breakdown of what happened and why markets reacted the way they did.

Microsoft Beats Earnings Expectations Across the Board

Microsoft reported its earnings for the quarter ending December 31, 2025, beating both revenue and earnings expectations, according to CNBC’s earnings coverage.

Key Financial Highlights (Q2 FY2026)

- Total Revenue: $81.3 billion, up 17% year over year, beating analyst estimates

- GAAP Net Income: $38.5 billion, a 60% YoY increase

- Non-GAAP Net Income: $30.9 billion, up 23% YoY

- Diluted Earnings Per Share (EPS): $5.16, above expectations of $4.95

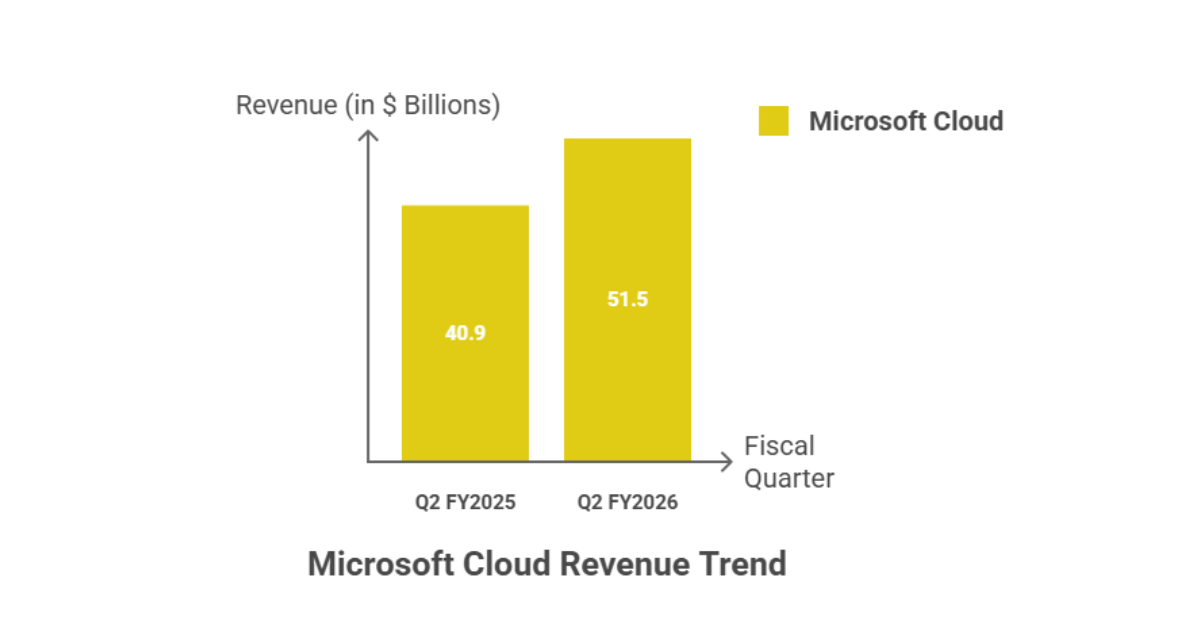

- Microsoft Cloud Revenue: $51.5 billion, up 26% YoY

CNBC reported that Microsoft’s earnings beat expectations on both the top and bottom lines, reinforcing the company’s position as one of the strongest performers among mega-cap tech stocks.

Cloud Revenue Crosses a Major Milestone

Microsoft’s cloud business once again proved to be the backbone of its growth story. According to Yahoo Finance’s earnings analysis, cloud revenue exceeded $50 billion for the first time, marking a major milestone.

What’s Driving Cloud Growth?

- Azure and other cloud services grew roughly 39% year over year

- Enterprise demand remained strong despite macro uncertainty

- Long-term contracts boosted visibility into future revenue

Microsoft also disclosed that its Remaining Performance Obligations (RPO) — future contracted revenue reached $625 billion, with approximately 45% tied to OpenAI-related commitments, as highlighted in a Yahoo Finance preview article.

Line chart showing cloud revenue growth from Q2 FY2025 ($40.9B) to Q2 FY2026 ($51.5B). This steady upward trend reinforces why investors continue to view Microsoft as a dominant force in enterprise cloud computing.

AI Spending Sparks Market Anxiety

Despite the strong numbers, Microsoft stock dropped 4–7% after hours, and the reason wasn’t revenue — it was spending.

According to MarketWatch’s post-earnings analysis, investors focused heavily on Microsoft’s rapidly rising AI-related capital expenditures.

AI and Capital Expenditure Breakdown

- Total Capital Expenditures: $37.5 billion in Q2 FY2026

Year-over-Year Increase: Approximately 66% - Spending primarily focused on:

- AI data centers

- GPU infrastructure

- Cloud expansion to support AI workloads

Yahoo Finance noted that while AI spending is strategic, it places short-term pressure on margins, which markets are increasingly sensitive to in the current rate environment.

Bar chart highlighting the sharp rise in AI-related spending, with Q2 FY2026 emphasized. This chart visually explains why investors reacted cautiously despite strong earnings.

Why Microsoft Stock Fell Despite Beating Estimates

The disconnect between earnings strength and stock performance becomes clearer when comparing actual results vs. expectations.

Earnings vs Market Expectations

| Metric | Actual | Expected | Market Reaction |

| Revenue | $81.3B | $80.1B | Stock down ~5% |

| EPS | $5.16 | $4.95 | Stock down ~5% |

| Cloud Revenue | $51.5B | $50.0B | Stock down ~5% |

MarketWatch explained that investors are now prioritizing future margin sustainability over near-term earnings beats.

Combination chart comparing earnings surprise with post-earnings stock decline

The message from markets is clear: growth alone is no longer enough execution and cost control matter just as much.

What This Means for Investors Going Forward

Microsoft’s earnings highlight a broader theme playing out across tech stocks.

Bullish Signals

- Cloud revenue growth remains strong and consistent

- Enterprise demand continues despite economic uncertainty

- AI investments strengthen Microsoft’s long-term competitive edge

Risks to Watch

- Rising AI costs may continue to pressure margins

- Investors want clearer timelines for AI monetization

- Stock volatility may persist as expectations reset

As MarketWatch emphasized, the market reaction reflects valuation discipline, not weakening fundamentals.

Microsoft’s Growth Is Intact But Expectations Are Higher

Microsoft’s Q2 earnings confirm that the company remains financially strong, with cloud revenue crossing $50 billion and profits exceeding expectations. However, rising AI-driven capital expenditures have shifted investor focus toward margins and future returns.

For long-term investors, Microsoft’s cloud and AI strategy remains compelling. For short-term traders, volatility driven by spending concerns may continue.

Stay with FinanceCurves for sharp, data-driven insights on tech earnings, AI trends, and market reactions.

FAQ

Why did Microsoft stock fall after Q2 FY2026 earnings

Despite beating expectations, investors reacted negatively to rising AI spending and margin pressure, according to MarketWatch.

How much did Microsoft make from cloud services?

Microsoft reported $51.5 billion in cloud revenue, up 26% year over year, per Yahoo Finance.

How fast is Azure growing?

Azure and other cloud services grew approximately 39% year over year.

Is Microsoft spending too much on AI?

Spending is high, but management views it as a long-term strategic investment rather than a short-term profit driver.

Is Microsoft still a strong long-term stock?

Fundamentals remain strong, but investors are closely watching execution, margins, and AI monetization timelines.

Disclaimer

The information provided on this website is for informational and educational purposes only. While we strive to ensure accuracy and keep our content up to date, FinanceCurves makes no guarantees regarding the completeness, reliability, or accuracy of any information published.

Nothing on this site constitutes financial, tax, legal, or investment advice. Readers should consult a qualified financial advisor, certified tax professional, or licensed attorney before making any financial decisions. Your individual situation may vary, and decisions based on information from this website are made at your own risk.

FinanceCurves may reference government agencies, financial institutions, or official programs for informational purposes only. We are not affiliated with, endorsed by, or connected to any government entity, including the IRS or any federal or state agency. Some content may contain links to third-party websites for additional context or resources. We are not responsible for the content, accuracy, or practices of any external sites.

By using this website, you agree to this disclaimer and our terms of use.

Marshall Mason, Senior Market Analyst at FinanceCurves.com, has over 9 years of experience covering financial markets, cryptocurrencies, and macroeconomic trends. He delivers data-driven insights, independent analysis, and actionable guidance for investors and traders. Marshall leverages authoritative sources, market data, and regulatory updates to help readers navigate volatility, adoption trends, and the evolving landscape of global finance and digital assets.